1 Make a list of your sources of income

In retirement, your money will likely come from several places, such as:

- 401(k) plans

- Defined benefit and other pension plans

- IRAs, personal savings, and investments

- Social Security

- Part-time work

- Home equity

- Inheritance

Make a list of all your sources, including how much you’ve saved or expect to receive. This can help you understand how much income you may have in retirement.

2 Consider combining your retirement accounts

If you have more than one IRA or retirement account, you might think about combining them. Having your retirement savings in one place can help make managing your money easier. A financial professional can help you understand your options and decide if combining accounts is right for you.1

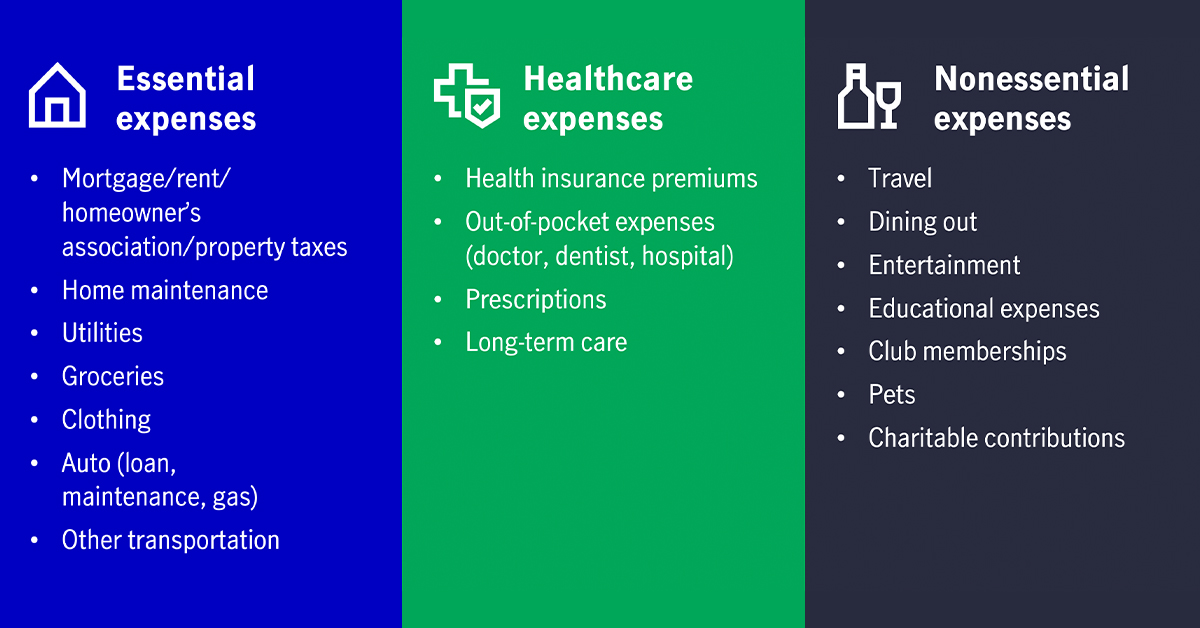

3 Set up a retirement budget

More than 50% of people ages 55 to 642 worry about running out of money in retirement. Having a budget can help you track your spending and manage expenses. Your spending will typically be higher in the beginning when you’re more likely to be active, travel, and eat out. It may then slow down for a bit, only to rise again, driven by healthcare expenses. Your retirement plan or IRA provider may offer tools to help you estimate your yearly spending and create a budget.

4 Create a plan to withdraw your money

Once you have your budget, the next step is deciding which accounts to take the money from to pay your expenses and in what order. This is called your withdrawal or drawdown strategy—and without one, your money might not last as long as you planned.

Here are a few common withdrawal strategies that can help you make the most of your savings, balancing your current and future financial needs.

At some point, you’ll be required to take a certain amount out of your 401(k) account and traditional IRA each year. These distributions are known as required minimum distributions, or RMDs. Make sure you include them in your plan as they can affect your withdrawal strategy.

5 Understand how taxes work

Not all of your income may be taxed the same in retirement. Some may be taxable, while others may be tax free. Understanding the difference can affect which accounts you tap first to help support your lifestyle.

- 401(k) plan—In many 401(k) plans, you have the choice of contributing pretax or after tax, or both. If you made pretax contributions, you’ll pay taxes on that money and any earnings when you take them out. If you contributed to a Roth 401(k), you can withdraw the money and any earnings tax free if certain conditions are met.3

- Defined benefit and other pension plans—Your plan may offer a choice of an annuity, which sends you a monthly payment, or a lump-sum withdrawal, which is paid all at once. These distributions are generally taxed when you receive them.

- Traditional IRA—You’ll owe taxes when you take money out.

- Roth IRA—You can withdraw your money tax free after age 59½ if certain conditions are met.4

- Personal investments—Depending on the investment, you may have to pay capital gains tax when you sell it.

You may want to work with a financial or tax professional to figure out your withdrawal and tax strategies. They can help you create a plan that works for your goals and personal situation.

Take time, then take your money

Your retirement savings may need to last 20, 30, or even 40 years. Having a plan can help you enjoy your time and stress less about money. In our 2025 financial resilience and longevity study, retirees with a formal plan for retirement felt significantly better about their financial situation than those without one (68% vs. 30%).5 Let their experience guide and inspire you to create yours today.

For more insight to help you thrive in retirement, check out our longevity hub.

FAQs

What’s the best withdrawal strategy for retirement?

The best strategy is the one that helps you meet your expenses and goals throughout your retirement. This strategy will be different for every individual.

In what order should you withdraw money from your retirement accounts?

You generally want to choose an order that helps minimize your taxes each year. That might mean tapping your taxable accounts first or your tax-free ones, or a combination of both. A tax professional can help you decide.

How much should you withdraw from your 401(k) each year?

There isn’t a one-size-fits-all amount that works for everyone. The answer depends on many factors, including your other sources of income, RMDs, and financial situation.

1 As other options are available, such as leaving it in your old plan, rolling over to an IRA, or cashing out, you are encouraged to review all of your options to determine if combining retirement accounts is suitable for you. 2 The Longevity Preparedness Index was developed in collaboration with MIT AgeLab and funded by John Hancock Life Insurance Company (U.S.A.). While financial support was provided for the research, it did not influence the findings, methodology, or conclusions. 3 A qualified distribution from a designated Roth account in the plan is a payment made after the participant attains age 59½ (or after death or disability) and after the designated Roth account in the plan has been established for at least five years. In general, in applying the five-year rule, count from January 1 of the year the first contribution was made to the designated Roth account. Participants should contact their plan consultant or financial or tax professional for specific details on the five-year rule and whether any special rule may apply. 4 A participant must satisfy the five-year holding period and either attain age 59½, die, or become disabled or become a first-time home buyer ($10,000 lifetime limit) in order to be eligible to receive a tax-free, qualified Roth distribution. 5 2025 Manulife John Hancock financial resilience and longevity report, a commissioned study.